Stop Foreclosure in Florida: 5 Strategies for 2026

Real Estate, Foreclosure Alternatives Florida, Florida Foreclosure Help 2026

How to Stop Foreclosure in Florida: 5 Proven Strategies (2026)

If you are behind on mortgage payments or just received a Notice of Default in Florida, you are not alone—and you are not out of options. This guide explains the Florida foreclosure timeline, five proven strategies to stop or avoid foreclosure, and how Fast 4 Cash Homes LLC can help you sell your house quickly to protect your credit, your equity, and your peace of mind in 2026.

Understanding the Florida Foreclosure Timeline in 2026

Knowing where you are in the process is the first step in deciding how to stop foreclosure in Florida. Florida is a judicial foreclosure state, which means the lender must sue you in court before your home can be sold. As of 2026, the full process typically takes 8 to 18 months from the first missed payment to the foreclosure auction, and in some contested cases it can stretch to 1–3 years (flforeclosurehelp.com; legalclarity.org).

Key Stages: Missed Payments → Notice of Default → Lis Pendens → Auction

- Missed Payments (Days 1–120): After a missed payment, you may get reminders and late fees. Around 90–120 days of delinquency, your lender usually sends a breach letter warning that the loan will be accelerated if you do not catch up (stateregstoday.com).

- Notice of Default & Federal Waiting Period (~Day 120): Federal law generally requires the servicer to wait at least 120 days of delinquency before starting a foreclosure lawsuit. During this time, you still have powerful options to get Florida foreclosure help 2026, including loan modification, repayment plans, or selling the property to avoid foreclosure (nolo.com).

- Lis Pendens & Lawsuit Filed (Around Months 4–6): The lender files a foreclosure complaint and a lis pendens in circuit court. This is the official beginning of the lawsuit and a public notice that your property is in foreclosure (flforeclosurehelp.com).

- Court Process & Final Judgment (Months 6–12+): You generally have 20–30 days to respond. If you do nothing, the lender can seek a quick judgment. If you fight the case or pursue loss mitigation, the process can stretch many more months, sometimes over two years in busy counties (flforeclosurehelp.com).

- Auction & No Redemption Period: Once the court enters a final judgment, it typically schedules a foreclosure sale within 20–35 days (flsenate.gov). After the sale and transfer of title, there is usually no post-sale redemption period for Florida mortgage foreclosures (miamidade.gov).

The earlier you act in this timeline, the more options you have. Even if a sale date is already set, it may still be possible to sell house to stop foreclosure or pursue other foreclosure alternatives Florida homeowners use every day.

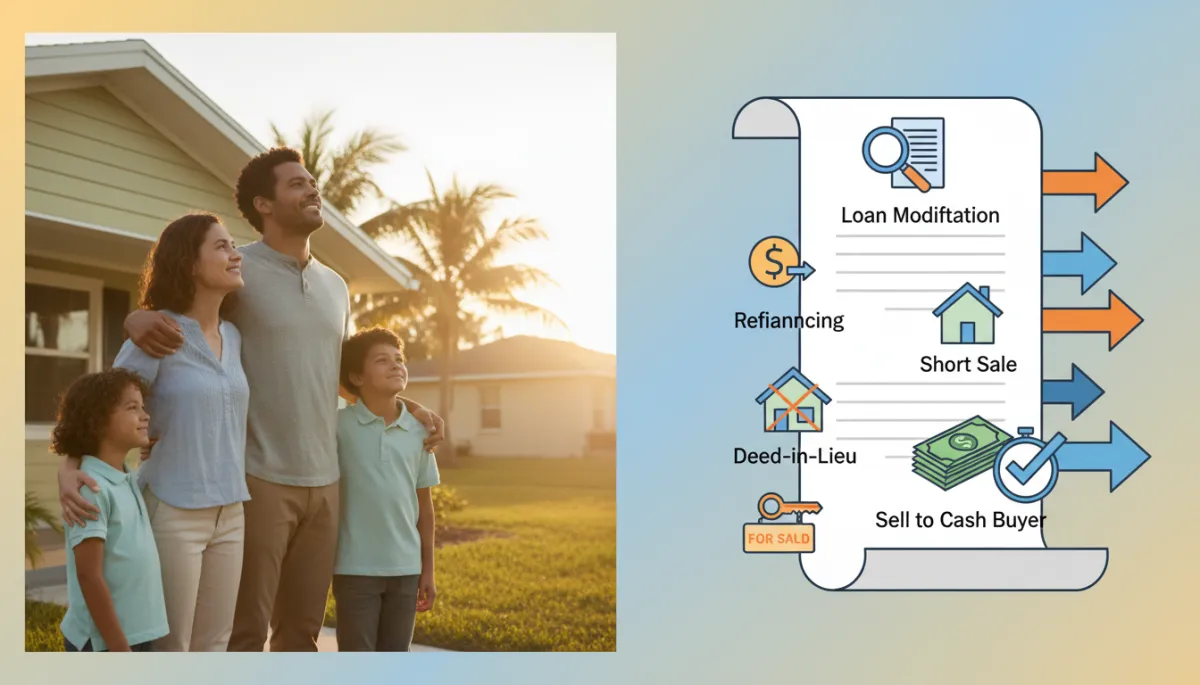

5 Proven Strategies to Stop or Avoid Foreclosure in Florida

1. Loan Modification

A loan modification changes the terms of your mortgage—such as interest rate, length of the loan, or adding missed payments to the back of the loan—to make your payment more affordable. This is one of the most common ways to get Florida foreclosure help 2026 and keep your home (consumerfinance.gov).

- Pros: You stay in your home; payment may be reduced; foreclosure is usually paused while your complete application is under review (“dual tracking” restrictions protect you in many cases).

- Cons: Approval is not guaranteed; the process can be slow; you must provide detailed income and hardship documents; if denied, you may be closer to auction with fewer options.

2. Refinancing Your Mortgage

Refinancing means replacing your current mortgage with a new one—ideally with a lower rate, longer term, or both. This can catch up missed payments and reset your loan, but it is usually only realistic before you fall too far behind and if your credit and income still qualify.

- Pros: You keep the home; may reduce monthly payment; can roll arrears into the new loan; may lock in better long-term terms if rates are favorable.

- Cons: Hard to qualify with recent late payments, job loss, or major credit damage; closing costs; takes time—often longer than you have if an auction date is already scheduled.

3. Short Sale

A short sale allows you to sell the property for less than the amount owed on the mortgage, with your lender’s approval. The lender accepts the sale proceeds and may forgive some or all of the remaining balance (consumerfinance.gov).

- Pros: Avoids foreclosure on your record; you may be able to negotiate a waiver of deficiency; gives you more control over your move-out timeline; can be less damaging to credit than a completed foreclosure.

- Cons: Requires lender approval; can take months; buyer financing can fall through; in some cases you may still owe a deficiency balance if the lender does not fully forgive the debt under Florida law.

4. Deed-in-Lieu of Foreclosure

With a deed-in-lieu of foreclosure, you voluntarily sign the property back to the lender in exchange for being released from the mortgage. This is often considered when the home has little or no equity and a sale is unlikely to cover the debt.

- Pros: Stops the foreclosure process; may reduce legal fees; sometimes includes relocation assistance (“cash for keys”); can be less public and stressful than a full foreclosure lawsuit.

- Cons: Lender must agree; usually only considered after attempts to sell have failed; you lose the home and any equity; depending on the agreement, a deficiency judgment may still be possible if not explicitly waived.

Local cash buyers can often stop foreclosure in days instead of months of uncertainty.

5. Sell to a Cash Buyer (Fast 4 Cash Homes LLC)

If you need to move quickly or your sale must close before a scheduled auction, selling to a reputable local cash buyer like Fast 4 Cash Homes LLC can be the fastest and most certain solution. We buy Florida houses in any condition, with or without equity, and work directly with your lender if there is an active foreclosure case.

- Pros: No showings, repairs, or appraisals; we can close in as little as 7–14 days in many cases; foreclosure can be stopped before auction; you avoid a foreclosure judgment on your record; you know your exact sale date and payout; we handle communication with the bank and the title company.

- Cons: You will no longer own the home; your net proceeds may be lower than a full retail sale—but often higher than losing the property to foreclosure and facing potential deficiency and credit damage.

Immediate Action Checklist When You Are Facing Foreclosure in Florida

When you are scared and stressed, it is easy to freeze. Use this checklist to take back control—one step at a time:

- Open every letter and email from your lender or the court. Ignoring notices will not make them go away and can shorten your options.

- Confirm exactly where you are in the foreclosure timeline. Have you only missed a few payments? Has a lis pendens been filed? Is there a sale date set? This determines which foreclosure alternatives Florida homeowners can still use.

- Call your lender’s loss mitigation department. Ask about loan modification, forbearance, repayment plans, or short sale options. Document every call, date, and person you speak with.

- Gather financial documents. Pay stubs, bank statements, tax returns, hardship letter, and a list of monthly expenses. You will need these for almost every option—modification, short sale, or deed-in-lieu.

- Consult a HUD-approved housing counselor or foreclosure attorney. A professional can explain your legal rights and help you compare options for how to stop foreclosure in Florida based on your exact situation (hud.gov).

- Evaluate whether you can realistically keep the home. Be honest about your income, future job prospects, and other debts. Sometimes the most caring decision for your family is a fresh start instead of a long, stressful fight to save a payment you cannot afford.

- Get a realistic sale option on the table. Talk to a real estate agent and a local cash buyer like Fast 4 Cash Homes LLC. Knowing what your house could sell for—and how fast—gives you leverage and clarity.

- If a sale date is already set, act with urgency. In many cases, selling your house to stop foreclosure is still possible, but every day counts once the auction is scheduled.

FAQ: Florida Foreclosure Help 2026

Can I sell my house to stop foreclosure in Florida?

Yes. In most cases, you can sell house to stop foreclosure at any point before the foreclosure auction actually occurs. If the sale proceeds are enough to pay off the mortgage and costs, the foreclosure is dismissed and there is no foreclosure judgment on your credit. Even if you are underwater, a short sale or a negotiated payoff with a cash buyer may still allow a sale that avoids an auction and reduces what you owe. Your lender must approve the payoff, but many are willing because it often costs them less than completing foreclosure.

How fast can a cash buyer close in Florida?

A genuine local cash buyer like Fast 4 Cash Homes LLC can often close in as little as 7–14 days, sometimes even faster if the title is clear and everyone can sign quickly. There is no waiting for bank financing, appraisals, or extensive inspections. This speed is critical if your foreclosure sale is only weeks away. In many 2026 cases, we are able to coordinate with the lender and the court so that the confirmed closing and payoff stop the foreclosure before the auction date.

Will I owe money after a short sale in Florida?

It depends on the agreement you reach with your lender. In a Florida short sale, the lender can choose to:

- Waive the deficiency (you owe nothing further); or

- Reserve the right to pursue a deficiency judgment for the remaining balance.

Before you sign any short sale approval letter, review it carefully with a foreclosure attorney or housing counselor. Make sure you understand whether the deficiency is being forgiven, settled for a smaller amount, or still collectible. When you work with Fast 4 Cash Homes LLC on a short sale or discounted payoff, we coordinate with your lender and your professional advisors to push for the most favorable terms possible.

Why Fast 4 Cash Homes LLC Is Often the Fastest Way to Stop Foreclosure

When you are behind on payments, every letter, phone call, and court notice can feel like a punch in the gut. Our mission at Fast 4 Cash Homes LLC is to provide clear information, compassionate guidance, and a real, workable solution—not pressure. For many Florida homeowners in 2026, selling to a cash buyer has been the quickest and least stressful way to end the foreclosure and move forward.

- We buy houses in any condition—no repairs, cleaning, or showings.

- We can make a fair cash offer within 24 hours of seeing the property.

- We often close in 7–14 days, or on the exact date you choose.

- We work directly with your lender, attorneys, and the title company to ensure the foreclosure is stopped and your loan is properly paid off or settled.

Take the Next Step Today: Talk to a Local Foreclosure Relief Team

You do not have to face this alone, and you do not have to wait until the auction to act. Whether you are just a month behind or already have a sale date on the calendar, there are still options for how to stop foreclosure in Florida and protect what matters most to you.

If you are ready to explore a fast, straightforward sale that can stop foreclosure immediately—without repairs, showings, or uncertainty—reach out to Fast 4 Cash Homes LLC today. We will listen to your situation, explain your options, and make a no-obligation cash offer so you can decide what is best for your family.

Call or text now: 727-261-2274

Get compassionate, local Florida foreclosure help 2026 and discover whether selling to a cash buyer is the right way for you to avoid auction, avoid a judgment, and move forward with peace of mind.